ANALYSIS: Japan's rates market sees liquidity boost on policy shift

9th April, 2026

An executive at Citigroup Global Markets Japan shares observations about the interest in the Japanese market and key US related regulatory issues banks are grappling with.

Shun Yanagisawa, director and Japan head for futures, clearing and FX prime brokerage at Citigroup Global Markets Japan, said that the Japanese yen swap and government bond futures are experiencing momentum, driven by the Bank of Japan's monetary policy normalisation.

"After raising the policy rate to 0.5% in January 2025 and further to 0.75% in December 2025, market volatility and trading activity have surged across both over-the-counter swaps and listed derivatives," said Yanagisawa.

Following two decades of zero and negative interest rates, Yanagisawa observed that yen swap clearing volumes have surged dramatically—up eightfold since 2021 to reach an average daily cleared volume of JPY 229 trillion (£1.09 trillion) in 2025, with a record single-day volume of JPY 146 trillion on December 4.

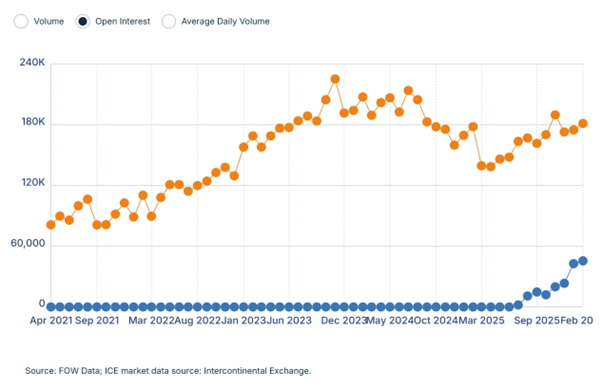

Open interest for 10-year Japanese government bond (JGB) futures has doubled since 2019, exceeding JPY 170 trillion by the end of 2025, while the long-dormant 20-year JGB futures contract was revived with open interest growing to over 40,000 lots by January 2026.

According to FOW data, open interest for 10-year JGB futures reached 181,292 lots in February 2026 while mini 20-year JGB futures open interest on OSE reached 45,526 lots.

Chart 1

10-year JGB and mini 20-year JGB futures open interest on OSE

Source: FOW data

While the three-month euroyen contract has traditionally been the big offshore market, futures haven't been popular among hedge funds.

"Euroyen futures have now changed to Tokyo overnight average rate futures after the interbank offered rate transition, but with lower margin compared with swaps, there's an incentive to trade more futures, particularly as longer tenor products such as the 20-year JGB futures gain traction," said Yanagisawa.

During a panel discussion at a major Tokyo seminar in February, Yanagisawa noted that speakers have observed a two-way flow return to the yen rates market after 20 years of suppressed volatility under yield curve control. The speakers said that the key is "ensuring domestic institutional investors return alongside the offshore players". With the approximate 80% holding by Bank of Japan of cheapest-to-deliver 10-year JGBs, liquidity remains a constraint.

Yanagisawa also said that the composition of Japan's yen swap market has undergone a dramatic shift.

"Non-resident participants, including both house and affiliate as well as client accounts, now account for 65% of cleared notional volumes as of Q4 2025, up from 44% in 2020," he explained.

In terms of regulatory developments, September 2025 saw a watershed moment when the US Commodity Futures Trading Commission issued a no-action letter permitting US persons to clear yen interest rate swaps through Japan Securities Clearing Corporation (JSCC) via non-futures commission merchants clearing members.

"This regulatory approval has leveled the playing field, allowing US hedge funds to access the deepest liquidity pool for JPY swaps alongside their non-US peers," said Yanagisawa.

As of January 2026, Yanagisawa said that six US customers have completed onboarding, and JSCC's total non-Japanese client base has expanded to 65 firms, including prominent names such as Citadel, Millennium, ExodusPoint and Garda.

In terms of regulatory changes to US Treasury repo markets, Yanagisawa said that Japanese banks are grappling with the US Securities and Exchange Commission's mandatory clearing rules.

They may require the head offices and non-US branches of Japanese banks to clear repo trades through a registered central counterparty (CCP) if the entire bank entity is deemed a “direct member” of the CCP. Compliance dates are set for June 30 2027.

"One solution to avoid the rules is to trade only with non-US counterparties who are not the direct members of the CCPs," said Yanagisawa. "However, the constraint for Japanese megabanks is that they usually have US branches as the direct members of the CCPs and would be captured by the regulation for repo transactions."

Yanagisawa noted that banks are preparing for the mandate but there remain issues around whether an agency or sponsor model should be used.

Under a sponsor model, the execution and clearing are done by the same counterparty while under an agency model, the relationship is separate with multiple counterparties.

"From a market infrastructure perspective, banks need to decide which to use and ensure that ecosystems are in place to match trades while navigating an area that is still unclear: accounting treatment," said Yanagisawa.

Related topics

Related Articles

All Insights8th July, 2026

SGX sells Scientific Beta to STOXX

Singapore Exchange (SGX Group) has agreed to sell its wholly owned index subsidiary Scientific Beta to Deutsche Boerse Group-owned global index provider STOXX.

Zak Jakubowski

8th July, 2026

Webull brings institutional platform targeting brokers, fintechs, hedge funds

The platform aims to provide brokerage infrastructure, clearing services, application programming interface (APIs) and embedded investing solutions to financial institutions worldwide.

Narayani Srinivasan

8th July, 2026

G.H. Financials clears first trades on ICE three-month TONA futures

The transaction marks a pivotal moment for the Japanese Yen (JPY) derivatives market, highlighting the growing competition among global exchanges to capitalise on increasing demand to manage short-term JPY interest rate exposure.

Narayani Srinivasan