ANALYSIS: ION rolls out pre-trade margin tool for CME SPAN 2

29th April, 2025

ION has gone live with an optimised margin tool which allows faster approximation of margin requirements under CME Group’s new “SPAN 2” methodology, giving traders the ability to manage portfolio risk in volatile market conditions.

ION’s XTP Risk JANUS service will now include the tool in its pre-trade Margin Engine, the London-based firm said on Tuesday. The move is the culmination of work by LIST, the trade analytics platform ION acquired in 2021, stretching back a year. LIST has had a dedicated financial engineering team looking at ways to leverage machine learning techniques to allow models to be deployed faster. The team identified a use case to the update of CME’s margin calculation model to SPAN 2, a phased process that went live for energy products in 2023 and equity derivatives in the second half of 2024, with further expansions planned. The updated model shifts to historical value-at-risk model that simulates wider risk scenarios and factors, increasing complexity.

“What we saw a year ago is that the large disparity between the margin models could cause issues – especially in times of volatile markets,” Mirko Marcadella, chief product and marketing officer at LIST told FOW. “It is a difficult balance to strike and becomes particularly acute for intraday processes that require timely outputs.

“When we started showing clients the results that could be achieved using artificial intelligence to accurately approximate SPAN2 in real-time, it became clear how important this could be for the wider industry. Beyond the pre-trade margin use case, clients can also perform rapid ‘what if’ analysis of portfolios to gauge sensitivity to large market moves.”

The LIST model, dubbed “DeepMargin” goes further than the SPAN 2 approximation tool made available by CME in early 2024. The CME tool reduces latency by taking the original methodology and expanding the underlying data to reflect the SPAN 2 risk array, making it available to clients on its platform. ION has been able to use the widely understood original SPAN margin to evaluate SPAN 2 requirements by training a neural network model on the difference between the methodologies. The data set is derived from randomly generated portfolios process at market close every week. The much faster SPAN outputs can then be used to predict SPAN 2 requirements.

“We now have a process that allows us to provide a trained machine to clients or provide the technology that lets the client train the machine on their own data,” Marcadella added. “We also provide the risk management tool that embeds the neural network calculation into pre-trade over validation for cleared derivatives trading.”

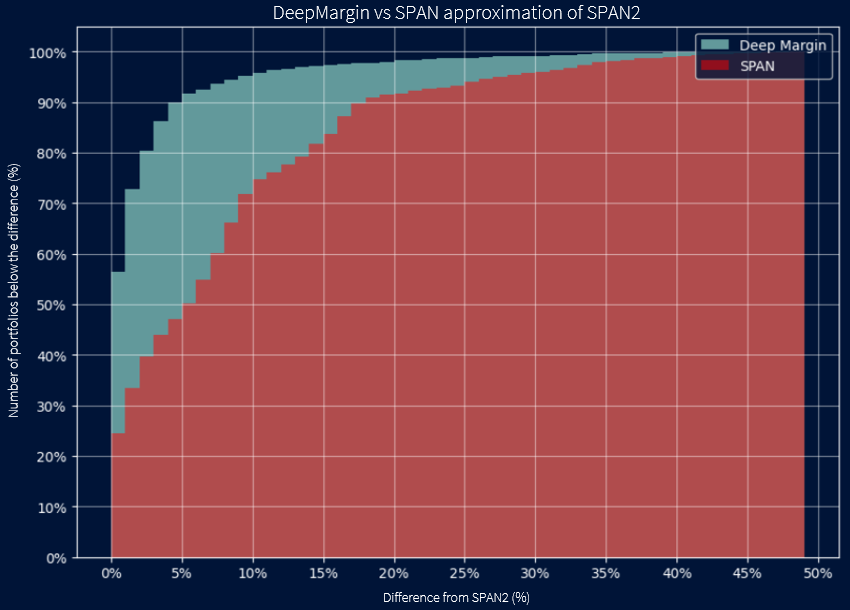

The model has performed well in testing, offering more accurate prediction of margin changes than the CME approximation tool. Based on a test data set of 10,000 portfolios not used for training, as shown in chart 1. The chart shows how much closer DeepMargin can infer margin requirements on tested portfolios against the public SPAN 2 approximation. For example, 90% of portfolios using DeepMargin had a five percent difference to the SPAN 2 output, versus only 45% using the CME approximation.

Chart 1

Source: LIST

“The DeepMargin model gives outputs that are far more accurate than the SPAN2 Approximation equivalent and crucially allows computation time to be completed in a few milliseconds versus seconds using the SPAN 2 library,” Riccardo Bernini, head of financial engineering and artificial intelligence at LIST said in an interview. “Further analysis has also shown that there is no degradation during the week as we move away from the weekly calibration periods for the engine.”

The release comes at a time of heightened volatility and trading in listed markets, as US tariff uncertainty has upended sentiment across regions. The CME at the start of April “proactively” increased margin requirements in various products in incremental steps to safeguard collateral, it said on a results call this month. It hit a new single day for moving cash related to mark-to-market positions on April 9, moving $32 billion (£23.9bn) between firms on that day according to figures cited by the exchange. That dwarfed the additional collateral related to margin increases on that day of $7 billion, it said.

As of the end of trading on April 21, US listed options average daily volume (ADV) for the year to that date was at 59.6 million contracts, boosted by a spike in trading in April as tariff uncertainty roiled markets. That means the market at this pace would reach around 15 billion contracts traded this year, well above last year’s record tally, according to data compiled by Cboe Global Markets.

Related topics

Related Articles

All Insights7th July, 2026

Tradeweb rates derivatives ADV jumps 59% in June

The electronic trading platform reported broad-based growth across rates, credit and ETF markets as automation and international client activity continued to drive volumes.

Zak Jakubowski

7th July, 2026

Eurex eyes Kraken launch for retail derivatives expansion this year

The Deutsche Boerse Group-owned venue expects to make its derivatives available through crypto exchange Kraken by the end of the year, as the exchange operator looks to broaden retail participation in regulated derivatives markets.

Zak Jakubowski

7th July, 2026

ICE assumes administration of LBMA platinum and palladium benchmarks

The move means ICE Benchmark Administration now oversees all four of the London Bullion Market Association's precious metals benchmarks and their daily price-setting auctions.

Zak Jakubowski