OPINION: From 'blast all' to 'select smart': How dealer selection is evolving

1st April, 2026

Over the past decade, the Request-for-Quote (RFQ) protocol has transformed US corporate bond trading. It was the first electronic trading protocol introduced in corporate credit and remains the dominant method of electronic trading in the market today, precisely because it delivers transparency, competition and scalability across a wide range of trade sizes. Clients turn to the RFQ protocol to streamline workflows and execute more trades simultaneously than was ever possible through traditional voice trading.

As the RFQ protocol evolved, clients increasingly adopted the “blast all” approach – sending RFQs to both disclosed dealers and anonymously, to the broader dealer and buyside network. The prevailing logic in electronic credit trading was straightforward: show the trade to as many counterparties as possible and more competition meant better pricing, faster execution, and greater confidence in outcomes.

This approach was supported by Tradeweb’s All-to-All (A2A) RFQ network, which grew significantly in recent years, with volumes up almost 300% between 2020 and 2025, reflecting how widely this model has been adopted across institutional credit markets. However, despite years of electronification, a meaningful portion of credit markets still rely on bilateral execution - particularly for larger, size-sensitive trades, with roughly half of the market continuing to trade over the phone, according to Coalition Greenwich research.

As electronic trading has matured, market participants are becoming more selective about how the RFQ protocol is used, particularly as trade size, liquidity and market conditions vary. Increasingly, AI and advanced data analytics are playing a role in this evolution, equipping traders with more precise insights into dealer behaviour, liquidity conditions and execution outcomes.

Balancing execution quality and market impact

The success of RFQ is rooted in transparency and competition. By sending inquiries to the entire dealer and buy side community, traders can solicit multiple quotes simultaneously, rather than calling dealers individually over the phone. For smaller and more liquid trades, this model works exceptionally well, while larger block trades remain concentrated in bilateral or voice channels. In this instance, clients hesitate to expose larger trades to the entire market, prioritising information leakage over potentially more competitive pricing.

More competition can sharpen quotes. But it also increases the amount of information revealed to the market. Once visible, that information has impact – it can influence subsequent pricing, hedging behaviour and liquidity across related instruments. By choosing voice execution, clients prioritise minimising market impact over the potential cost savings from broader competition. Conversely, an A2A RFQ increases the chance of lower transaction cost but comes at the expense of wider information dissemination.

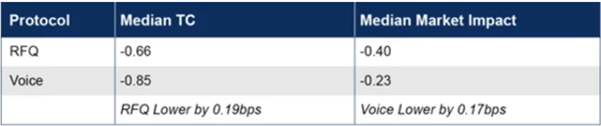

Tradeweb analysis of investment grade (IG) trades above $1m (£753k) executed on the platform in 2025 (see table 1) shows that broader A2A RFQs deliver approximately 0.2 basis points (bps) of improved execution quality relative to comparable voice trades. However, broader distribution comes with measurable trade-offs. Using Tradeweb’s Ai-Price data and delayed spotting technology, we found that A2A RFQs exhibit roughly 0.17 basis points higher market impact relative to voice trades. (Stay tuned for a more in-depth study on measuring market impact, coming soon).

Table 1: Median transaction costs and market impact by protocol

Source: Tradeweb

Taken together, these findings (see table 1) illustrate a structural balance: broader RFQ distribution can improve execution pricing but may also increase market impact – particularly as trade size increases.

A more data-driven approach to dealer selection

In practice, only a subset of dealers consistently win large size RFQs, suggesting that broad distribution is not always necessary to achieve competitive outcomes. This means clients may not need to “blast all” to achieve strong execution on larger trades.

Currently, clients are faced with two extremes: they either must trade bilaterally on their larger sizes to reduce information leakage and minimise market impact, or trade A2A on their smaller sizes to increase the chances of the most competitive response. To solve for this, Tradeweb has developed SNAP+ dealer selection functionality. This allows traders to dynamically select dealers that are statistically more likely to engage and win a given inquiry based on criteria such as historical performance and intraday trading activity, without the need to expose the trade to the entire market.

What’s more, this new functionality creates a middle ground between bilateral voice execution and full A2A distribution – maintaining competition while reducing information leakage for larger trades. Clients remain fully in control and can add or remove dealers from any recommended list, combining long-standing relationships with data-driven insight.

A smarter approach to liquidity

More broadly, this reflects a continued evolution in credit market structure – where participants are no longer forced to choose between information control and competitive pricing. Instead, data-driven dealer selection is enabling a more efficient matching of liquidity, particularly for trades that have historically sat between fully bilateral and widely distributed workflows. Underpinning this shift is the growing use of AI-driven analytics, enabling more intelligent dealer selection based on historical performance and real-time market signals.

As electronification in credit continues to evolve, this shift toward more intentional, data-driven execution is becoming increasingly important. Rather than relying on broader distribution to source liquidity, traders can now engage it with greater precision. Within this landscape, Tradeweb brings together the full spectrum of execution protocols – from voice processing for larger sized block trades, to A2A RFQ, and now the addition of SNAP+ - providing a more complete and flexible solution for client inquiry.

Co-authored by Harveer Mahajan, director, US credit, Tradeweb.

Data analysis by Anastasia Demina, vice president, US credit, Tradeweb.

Related topics

Related Articles

All Insights30th June, 2026

Wedbush joins DraftKings, Kraken in prediction markets push

The California-based broker has announced membership in DraftKings’ proprietary exchange and Bitnomial Clearinghouse to expand multi-asset clearing and execution capabilities across regulated prediction markets and digital asset derivatives.

Aravind Bulusu

30th June, 2026

Options Technology launches AtlasInsight V5 for advanced analytics

The fintech said the latest version of its flagship market data platform represents a boost to functionality and performance.

Aravind Bulusu

30th June, 2026

CME looks to product development to harness hedging demand

CME Group sees an enhanced product suite driving volume and open interest growth, as traders look to refine strategies in the face of volatile commodity markets.

Radi Khasawneh